Exploratory Data Analysis

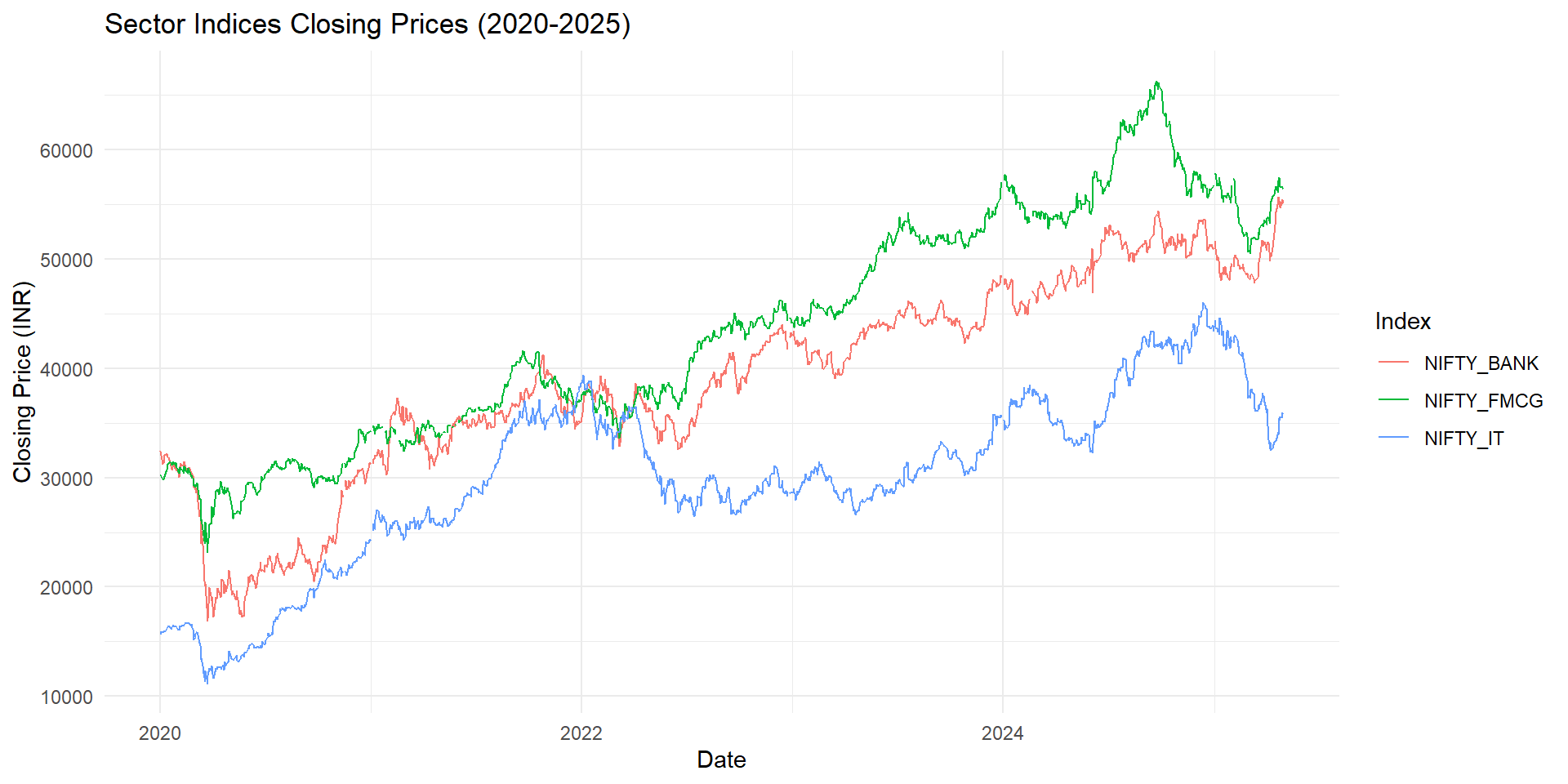

2. Overall Trend in Sector Indices

Interpretation: All sectors show upward trends with some volatility, especially Banking.

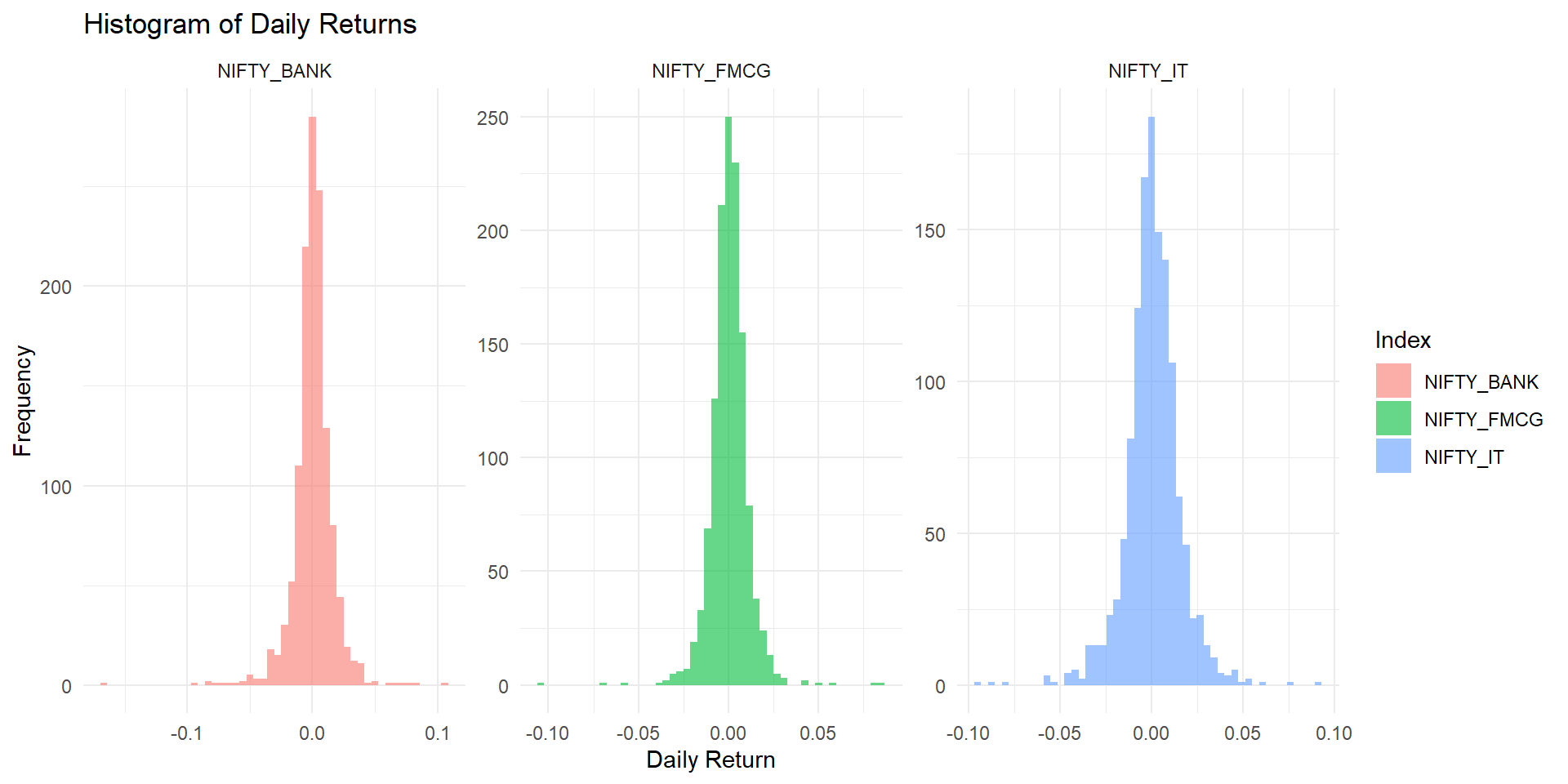

4. Distribution of Daily Returns

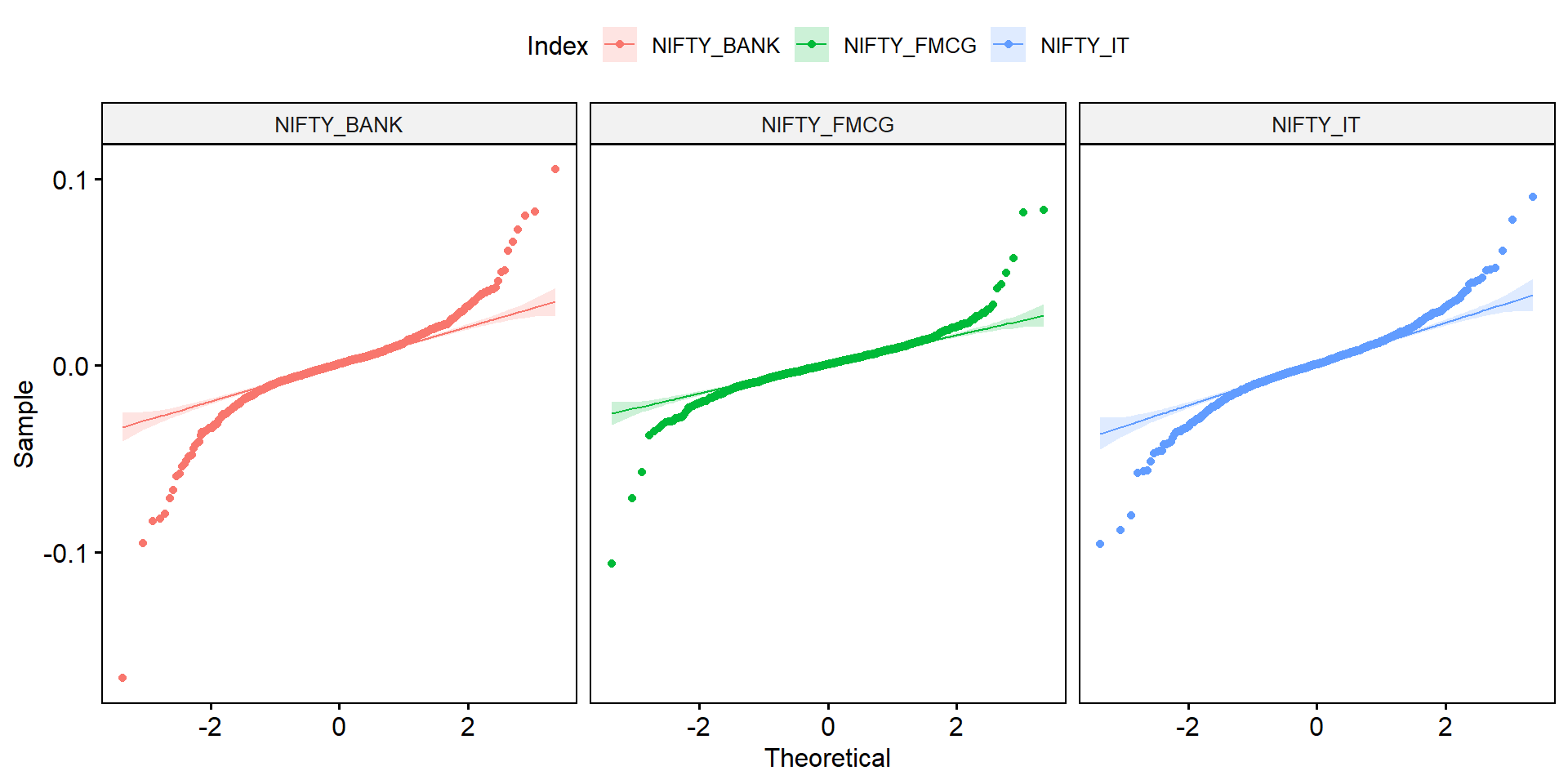

5. Normality Check with QQ Plot

Interpretation: Returns show deviation from perfect normality, common in financial data.

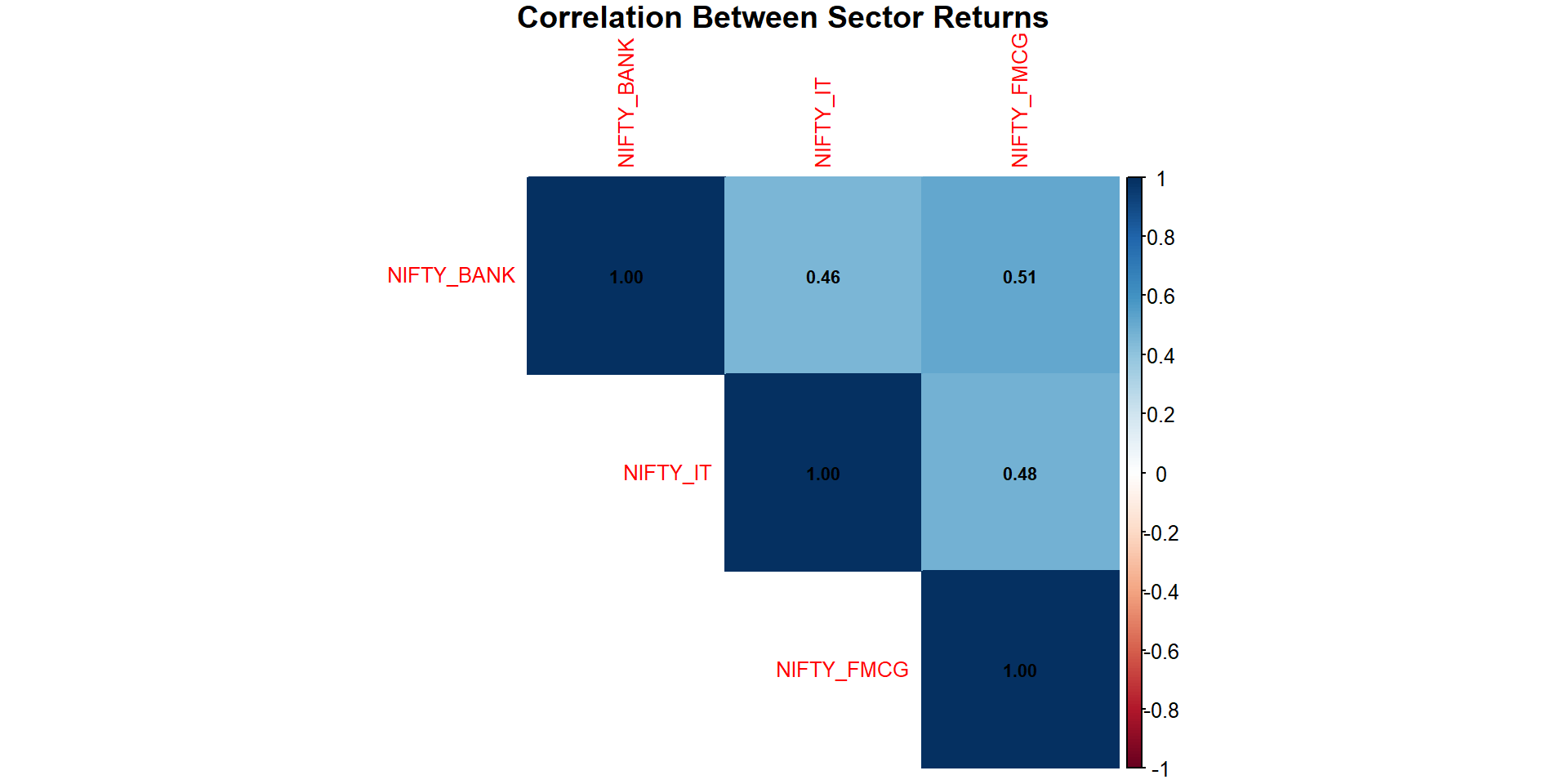

7. Correlation Analysis

# Reshape returns to wide format

returns_wide <- sector_returns %>%

select(Date, Index, Return) %>%

pivot_wider(names_from = Index, values_from = Return)

# Correlation matrix

cor_matrix <- cor(returns_wide %>% select(-Date), use = "complete.obs")

# Correlation plot

corrplot(cor_matrix, method = "color", type = "upper",

addCoef.col = "black", tl.cex = 0.8, number.cex = 0.7,

title = "Correlation Between Sector Returns", mar = c(0,0,1,0))

Interpretation: Positive correlations imply that sectors often move together. Banking and IT sectors show moderate correlation.